Alpha Metallurgical Stock: Debt Free And Printing Cash (NYSE:AMR)

Monty Rakusen

Alpha Metallurgical Resources Alpha Metallurgical Resources Alpha Metallurgical ResourcesNYSE:AMR), a leading player in the Metallurgical Coal industry, stands out in today’s investment landscape due to its straightforward business model and dedication to shareholder returns. The company’s recent financial discipline has been a testament to its ability to withstand volatile market conditions. Buyback of stock, increasing shareholder dividends, and reducing debt to almost zero.

At the moment, the company’s stock is trading at a relatively attractive price, and also in comparison to previous levels. We see this as presenting us with a great opportunity.

Let’s jump in.

Financial Results

AMR’s financial performance over the past few years shows a mix of strengths, challenges and a positive overall trend.

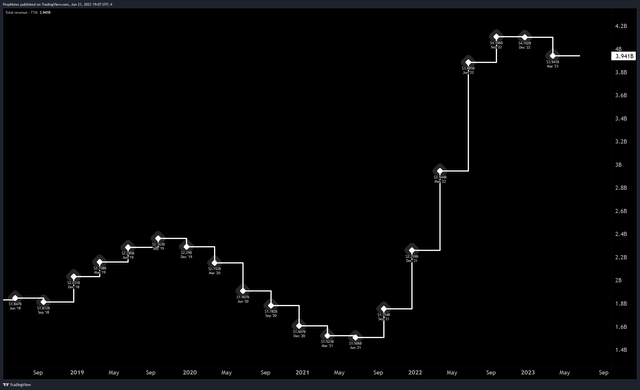

The company’s top line has grown strongly, with TTM revenues soaring by 34% to $3.94 Billion, an increase of 34% year-over-year.

TradingView

The main reason for this is the increased demand for coal, which has resulted from A limited supply response and improved economic activity are two factors that have contributed to the improvement in economic activity. Although the TTM chart appears to be a great one, there are some recent issues.

The company reported only $911 million sales in their latest quarter. This translates to $3.4 billion revenue per year, a decrease from the previous period.

In its most recent 10-Q, company said the following:

For the three months ending March 31, 2020, coal revenues fell by $163.0 Million, or 15%, from the previous year period. The decrease in coal revenues was due to lower coal realizations within the Met segment. Prices have moderated since the previous year.

The company is basically saying that 2022 was a very hot year, but 2023 will be a bit more moderate. It makes sense to look at the long term trends in sales for both the company and its competitors.

Met Coal demand should be boosted by an expected increase in steel production.

The World Steel Association’s (“WSA”) most recent Short Range Outlook projects a 2.3% rebound in steel demand this year, bringing expected global demand to 1.82 billion metric tons. The organization anticipates a steel demand of 1,85 billion metric tonnes in 2024. A further increase of 1.7% is expected, led likely by manufacturing, and accelerating in most regions. China will, however, see a slowdown due to population decrease.

The overall demand profile for AMR’s end product seems to be holding up fairly well, despite some moderating factors.

What we need to know is what AMR did with their recent success.

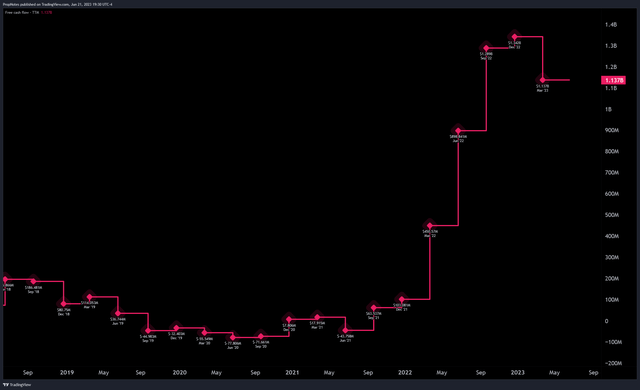

The cash flow statement of AMR is shown below:

TradingView

You can see that the company spent its free cash flow in the last six quarters to buy back stock worth more than $660,000,000, pay off nearly all the $470,000,000 of debt and pay just under $100,000,000 in dividends.

The company has taken home 1,13 billion dollars in free cash flow during the past 12 months.

TradingView

Consider the entire picture. You’ve got an organization with virtually no debt and solid FCF (Financial Cash Flow) margins of around 29%. There is minimal capex needed in the core business.

There will be bumps in the road, but the company has a great future and is well-positioned to deliver returns to its shareholders.

After tax, after the revenue is received, the company has a 34% operating profit margin, which includes all operating costs, CAPEX and depreciation. The remaining money goes to dividends and buybacks. No debts to pay, no big capital expenses, and a streamlined & straightforward basis for returns.

Last but not least, many people view coal as an industry in perpetual decline. AMR’s Met Coal is doing well and should continue to be able to return capital to its shareholders for many years to come. Met Coal stands out from Thermal Coal which is only produced as a by-product and only accounts for 10% of the company’s revenue. Thermal Coal’s demand is declining, while Met Coal continues to be in high-demand.

Valuation

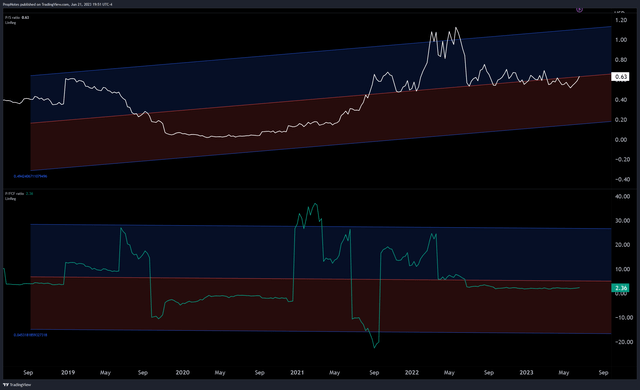

AMR appears attractive in terms of valuation. AMR is currently trading at a multiple of free cash flow of 2.3x and 0.69x. This seems to be a very attractive price.

TradingView

If you look closely at the historical value of a company, it is possible that its current market price does not reflect its true intrinsic value.

At these prices, it is clear that the market anticipates a significant fall in Met Coal’s prices. This would reduce margins, particularly compared to AMR’s fixed cost basis. This would reduce the immediate capital return to shareholders. As we have said, we believe the market is wrong about this stock because global steel demand will grow this year and into the future.

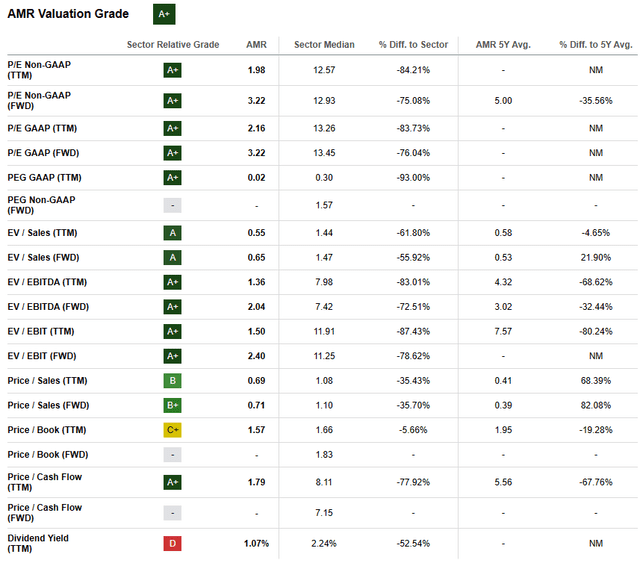

AMR is priced too high compared to itself and its industry:

SeekingAlpha

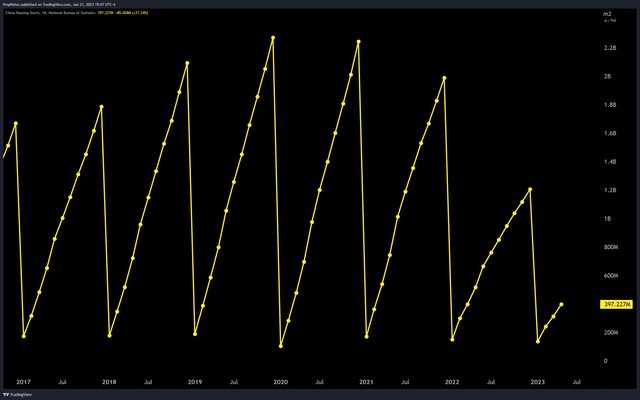

Chinese housing is the only negative aspect to mention.

TradingView

China has long been a major source of steel demand, but the numbers are terrible. The company has already fallen 119 million square metres behind what it was at this time last. And the trend is to get worse.

If things worsen in China, it is not clear whether the rest of world will be able to pick up the demand for steel if China’s situation gets worse. This is primarily a problem that steel companies will have to deal with, but it could affect the prices of inputs such as Met Coal.

We believe that the current market valuation of AMR is wildly undervalued, given the company’s streamlined model and potential for total returns. The company could be rated higher.

Risks

We think that the stock setup is excellent, but it’s important to understand the risks of owning this company. The following are some of the main risks to consider:

MacroAMR faces broader macroeconomic risk, such as economic downturns or changes in government policy which could affect the coal industry.

ExecutionIf the company does not execute well, or if costs are allowed to spiral out of control, margins can shrink dramatically, which will affect the capital returns for shareholders and the stock price.

Commodity-linkedAMR’s revenue is based on the Met Coal price. Volatility of this commodity’s price can directly affect the company’s profit and ultimately its stock price.

Technical SentimentsThe stock is strong, going from a recent low of $3 to a recent range high of $183. The company has changed dramatically since 2020. Some may still think the stock is overbought in the long-term, making it difficult to make gains near term.

The following is a summary of the information that you will find on this page.

Alpha Metallurgical Resources, in summary, offers a compelling investment opportunity to investors looking to benefit from the company’s streamlined business models, debt-free standing, and solid profit margins.

AMR presents an excellent investment opportunity. With a price well below the historical average, a reasonable entry point for the stock, a potential return on total capital, and an appropriate balance between risk and reward, AMR represents a sound investment.